Weighing the pros and cons of buying versus renting a property is crucial for making a sound financial decision. In Australia, this choice is particularly pertinent, given the varying property markets across the country.

Whether you’re drawn to the stability of homeownership or the flexibility of renting, understanding the positives and negatives of each option is crucial for making an informed decision. Let’s explore the financial implications, lifestyle factors, and market conditions unique to Australia, helping you determine which path aligns best with your personal and financial goals.

Financial factors to consider

Cost of buying a property in Australia

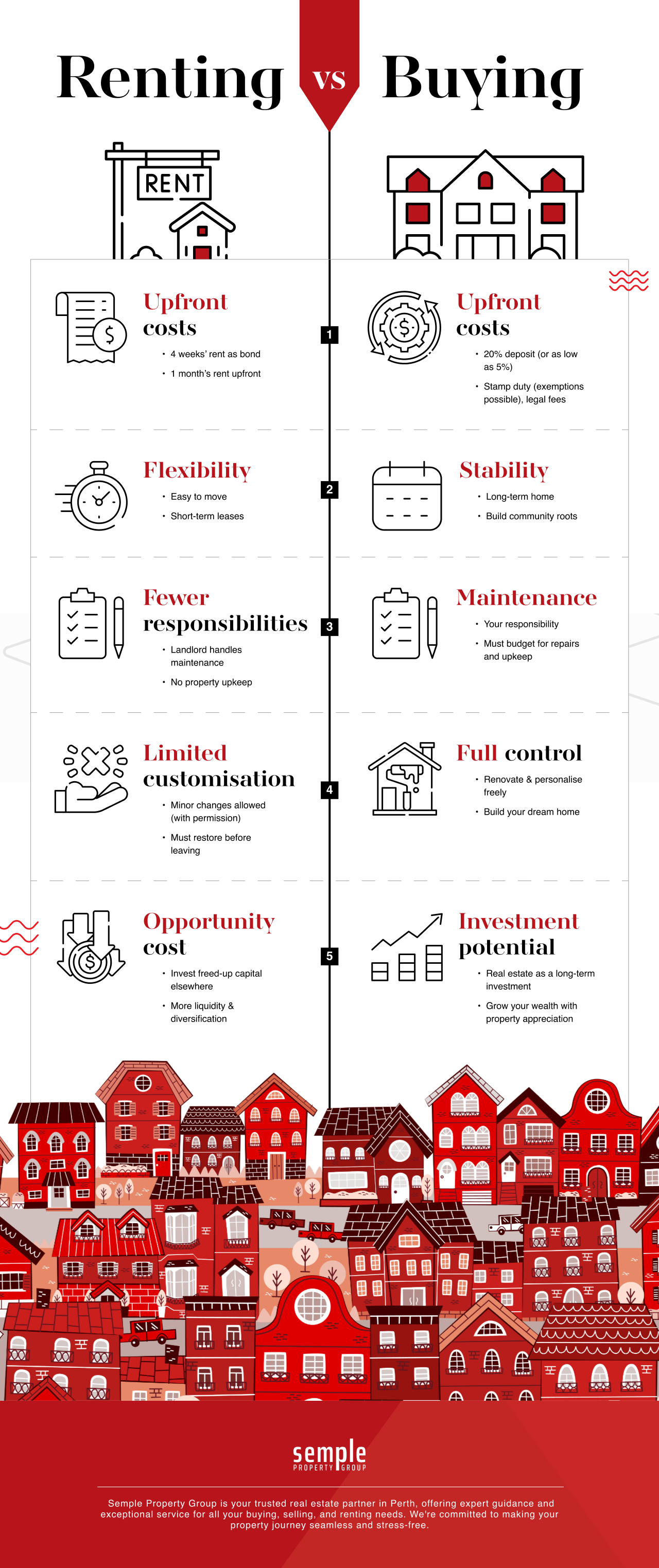

- Initial costs:

- Deposit: Typically, a 20% deposit is required, but several grants and schemes can significantly reduce this amount. For instance, the First Home Guarantee allows eligible buyers to secure a home with as little as a 5% deposit without paying Lenders Mortgage Insurance (LMI).

- Transfer Duty (Stamp Duty): First home buyers may be exempt from stamp duty or receive concessions. For example, in Western Australia, eligible buyers can receive an exemption for homes valued under $430,000 and concessions for homes valued between $430,001 and $530,000.

- Other costs: include legal fees, building inspections, and mortgage establishment fees.

- Ongoing costs:

- Mortgage payments

- Council rates

- Strata fees (only applicable for units or apartments)

- Maintenance

- Home insurance

Cost of renting a property in Australia

- Initial costs:

- Bond: Typically worth four weeks’ rent as a security deposit.

- Advance rent: Usually two weeks rent paid upfront.

- Ongoing costs:

- Rental payments

- Utilities

- Basic contents insurance (optional)

Lifestyle factors to consider

Flexibility vs. Stability

-

- Renting: Offers significant flexibility, allowing tenants to move with relative ease. This is particularly beneficial for those who frequently relocate for work or personal reasons, as leases can be short-term and there are fewer long-term commitments.

- Buying: Provides stability and a sense of permanence. Homeowners can settle into a community, make long-term plans, and build equity in their property. This stability is ideal for those looking to establish roots and avoid the uncertainties of renting.

Personalisation

-

- Renting: Traditionally, renting has come with limitations on customisation. However, recent changes in Western Australia’s rental laws have made it easier for tenants to make minor modifications. These modifications can include hanging pictures, installing shelves, or other non-structural changes. Tenants still need to restore the property to its original condition upon moving out.

- Buying: Homeowners enjoy complete freedom to personalise and renovate their property as they see fit. Whether it’s painting walls, remodelling kitchens, or adding extensions, owners can customise their home to match their vision. However, for larger projects, it’s essential to check with local councils regarding permits and restrictions to ensure compliance with local laws.

Mobility

-

- Renting: Makes moving easier and less costly. Ending a lease, while involving some logistical considerations, is generally simpler and quicker than selling a home. This is advantageous for those who value the ability to relocate quickly.

- Buying: Moving as a homeowner involves selling the property, which can be a lengthy and expensive process. This reduced mobility can be a disadvantage for those whose circumstances may change unexpectedly, requiring them to move.

Maintenance and responsibilities

-

- Renting: Renting offers more freedom and flexibility with time and finances. Tenants generally rely on landlords for maintenance and repairs, meaning fewer responsibilities and unexpected expenses. This can be ideal for those who prefer a hassle-free living arrangement without the need to budget for ongoing property upkeep.

- Buying: Homeowners are responsible for all maintenance and repairs, from routine tasks like lawn care to major fixes such as roof repairs. It’s essential to budget 1-3% of the home’s purchase price annually for these costs. While homeowners have full freedom to customise their property, larger projects may require checking with local councils for necessary permits.

Market conditions

Current real estate market in Perth

The real estate market in Perth is currently characterised by a very tight rental market, with one of the lowest vacancy rates in Australia. As of early 2024, the rental vacancy rate in Perth has dropped to an astonishing 0.4%, making it extremely challenging for tenants to secure rental properties.

What impact does this have on buying vs. renting?

- For renters: The current rental market conditions in Perth can be daunting for prospective tenants. The high demand and low supply mean that rental prices have been increasing significantly. For instance, the median weekly rent for houses has risen to $640, while units have reached $580. This competitive environment makes renting a less attractive option for those who can afford to buy, as securing a rental property can be stressful and costly.

- For buyers: The challenging rental market conditions can make buying a more appealing option. Despite the upfront costs associated with purchasing a home, the long-term benefits of stable housing costs and potential property appreciation can outweigh the initial expenses. Additionally, first-home buyers in Western Australia can take advantage of various grants and schemes, such as the First Home Owner Grant and the First Home Guarantee, which can significantly reduce the initial financial burden.

Investment potential

Building equity through homeownership

One of the most significant advantages of homeownership is building equity. When you buy a home, your monthly mortgage payments contribute to reducing your loan balance, increasing your ownership stake in the property. Over time, as you pay down your mortgage and the property appreciates in value, your equity grows. This equity can be a substantial financial asset, providing you with options for future borrowing, investment, or even funding major expenses like retirement.

Real estate as a long-term investment

Real estate has historically been a robust long-term investment. Properties generally appreciate over time, offering potential capital gains. In Perth, property values have seen significant growth, with residential property values increasing by 16.7% over the past year alone. This trend suggests that investing in real estate can yield substantial returns over the long term, particularly in markets with strong demand and limited supply.

Opportunity costs and potential financial gains of renting and investing elsewhere

While homeownership has its benefits, renting can also be financially advantageous, particularly when considering opportunity costs. Renting may free up capital that can be invested elsewhere, potentially yielding higher returns than real estate. For example, investing in stocks, bonds, or other financial instruments can offer diversification and liquidity, which real estate investments typically lack.

Find your dream home with confidence

After reading through these points, hopefully you should have a clearer idea of whether buying or renting is the best option for you right now.

At Semple Property Group, your trusted real estate agency in Perth, we’re here to help you navigate these choices. Whether you’re looking to purchase a property and build your dream home or seeking rental properties that suit your lifestyle, we have the expertise and listings to meet your needs. Contact us today to explore your options and find the perfect home for you.

Related Articles

Where to change addresses when moving house

Where to eat in Perth - our top picks

Loud tenants? Here’s how to handle them

Switch to Semple

Let’s Do It Right Now!

Get in touch